/banner-2020/HSBC-Private-Banking---Detail-shot-of-modern-architecture-hotel-facade.jpg)

Blog Series: Equity Markets - Neither a Cynic nor a Sentimentalist Be

In Oscar Wilde’s play, Lady Windermere’s Fan, he describes a cynic as “a man who knows the price of everything and the value of nothing” while a sentimentalist is “a man who sees an absurd value in everything and doesn’t know the market price of any single thing”.

With some slight adjustments1, these characters could reflect the concerns equity investors face today – have cynics (growth investors) driven markets to full valuations or are sentimentalists (value investors) trying to maintain their sails after the wind has changed? The answer is yes, and no.

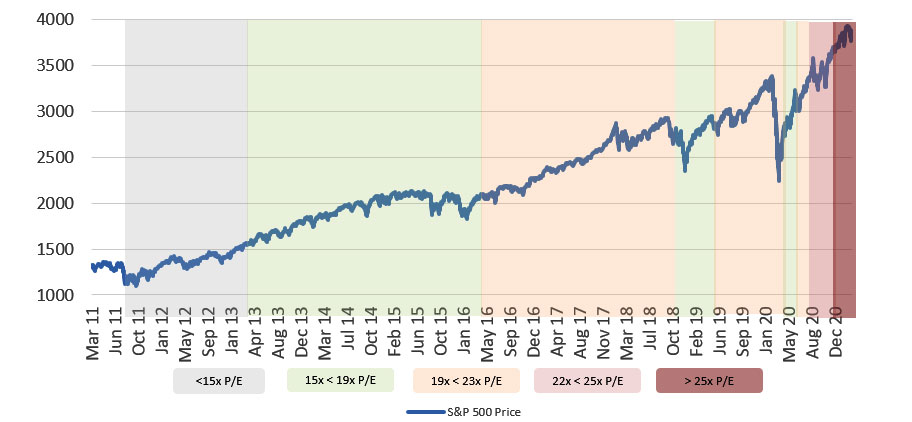

Valuations are certainly elevated (see below graph) and our recent note, A Deep Dive into Equity Valuations and Opportunities for Investors explores some of the structural reasons why this is so but we expect to see good value opportunities still available, across a range of price levels.

S&P 500 10 Year P/E Ranges

Source: Bloomberg L.P., HSBC Private Banking, 12th March 2021

The cynics and sentimentalists of today’s markets say that companies are either creating the future where no price is too high to take part or the business model is doomed to be disrupted out of existence. No alternate futures are suggested. We suggest though, that there is a middle ground, between the cynics and sentimentalists, of healthy investment opportunities at good prices. To access them however, you need to take yourself out of the noise and excitement, step back, separate narratives from fundamentals and focus on the opportunities. You may also need to leave behind some preconceptions of what investing success looks like and where it can be found.

Opportunities can be broadly categorised into the following:

- High Priced But Still Opportunities – These are companies in the universe trading on extended valuations but they are still attractive growth opportunities. This is particularly true when it comes to next generation technology in industries such as in healthcare, communications, transport and industrial robotics. The pandemic has accelerated many trends and many markets are in full transition, being disrupted completely (sentimentalists rejoice!). Undoubtedly, as a result of this, pre-pandemic corporate investment plans have been reset and will be redirected from pre-pandemic objectives as the weaknesses in many supply chains and processes are now known to need future proofing.

- Relative Value - These companies are ones that are growing well and also form part of growing sectors but are priced at a discount to their markets. Emerging Markets is a space that may contain more of these names as the adoption of technology and ecommerce in particular can move at a faster pace than in developed markets. For example, e-commerce penetration in the US is c.20 per cent while in China it is closer to 50 per cent.

- Absolute Value – these are opportunities that would fit into an absolute value approach where the book value and earnings ratios combine to offer an attractive investment opportunity with a much greater margin of safety than the high market fliers. A global approach is sensible for these companies but with a focus on emerging markets too as these markets are less scrutinized and so value opportunities have a greater chance of being available.

Emerging markets, which many investors still shy away from, have many tailwinds not enjoyed in developed markets such as average working age, sovereign and citizen debt profiles, technology adoption and market size. Enjoying less of the capital flows globally than developed markets, they have a larger set of opportunities which, when combined with their macro tailwinds, makes for an attractive mix. Some of the names in the above categories are also likely to be found in sectors that may have been nascent sectors over the last few decades and taking the time to learn about how some of these fringe sectors are developing will open the door to many opportunities that would not have been seen in otherwise.

Although markets are broadly in more expensive territory there is still opportunity available to the investor who can build out their sector and regional understanding. This can only be achieved by taking themselves away from the crowds, away from the noise, and away from the click friendly spectacle of the cynics and sentimentalists.

1i.e. a man who sees an absurd value in everything below their preferred P/E or P/B and doesn’t want to know the market price of any other single thing ↩