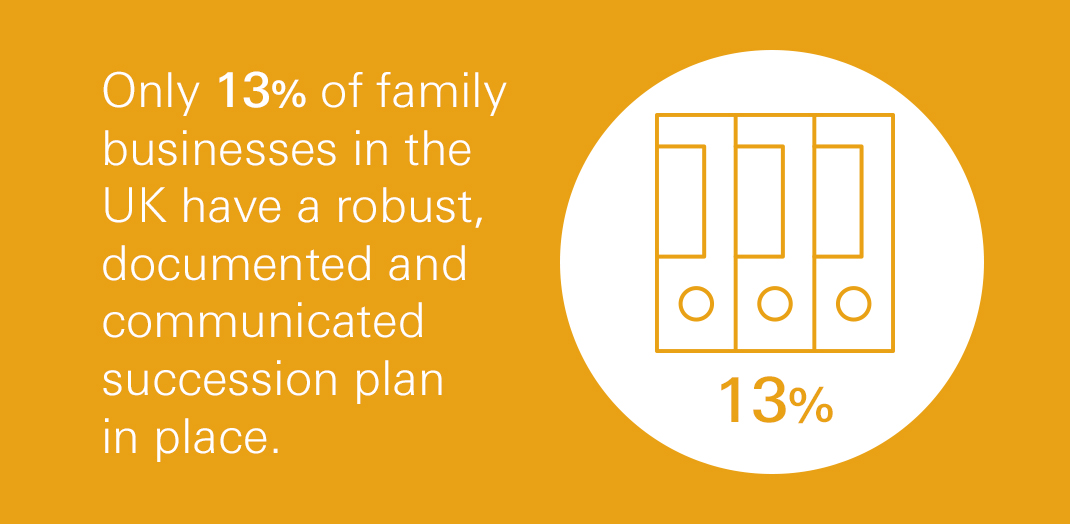

Five steps for continuing your family business

Shirtsleeves and back to shirtsleeves in three generations? How do you help your family enterprise, the combination of your family and the family business, avoid the cliché of rags to riches to rags?

Whatever your business, there are five things you can be doing now to avoid the gradual destruction of family wealth and, just as importantly, to ensure you and your future generations achieve the outcomes you want.

1. Prepare for change

Many family businesses fail, not because they don't have a good overall strategy, but because they haven't considered how the business will change as it and the family grow. There's something intrinsically organic about the growth of a family business and this sometimes leads to a lack of planning for the future.

Preparing for change, however, makes you more resilient, more in control. There are many possibilities to consider, for example, a younger family member joining the firm may bring new ideas or suggestions to enter new markets. How will the family enterprise cope with the loss of the family leader? How will you adapt decision making as the size of the family grows?

2. Keep a close eye on assets

One key reason why many family businesses don't survive beyond three generations is that the core assets become fragmented. This can happen because the number of family members grows rapidly and the family's wealth is split between them. It can also happen because of family relationship breakdown, such as a family member wanting to go their own way, or through divorce. Every family enterprise should have a strong vision backed up by a consistent and coherent strategy, which plans for issues such as these.

3. Tackle conflict before it happens

As a family and its business expands, so too does the opportunity for disagreement. Having mechanisms in place to deal with the conflicts that arise all too often in a family enterprise makes great sense.

A vital component in preparing for and tackling this challenge is a robust family governance framework. This sets out the details of family ownership, governance and management before a problem comes up.

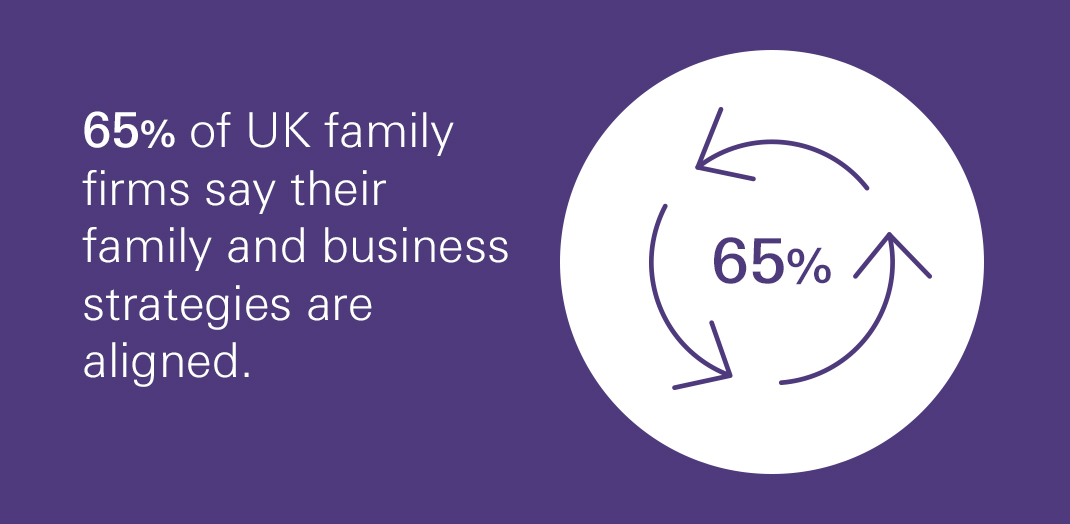

4. Never assume you're on the same page

When a business is made up of just two or three family members, communication and decision making are concentrated and are likely to happen informally. As the family and the business grow, you're more likely to need to work together with more formality. It's helpful if you can identify and define a shared purpose. And it's equally helpful if you can understand the way you will approach and take key decisions. These matters can be documented in a set of protocols – the family's code of conduct. This code can guide every member's dealings with each other and with the family enterprise.

A family is much more likely to abide by its code of conduct if everyone is involved in arriving at an approach that takes into account their views, aspirations, capabilities and needs.

5. Don't be wary of outside help

It's not always easy to make fundamental changes or draw up shared processes from within the family structure itself. It's not an admission of failure to get objective outside help to create the family governance framework and code of conduct.

Check with your relationship manager if this is an area of interest for you. It's a process that should begin with an understanding of the family's vision for their wealth and assets, and will almost always involve a series of family workshops to ensure development of the plan is 'owned' by family members.