/banner-2023/HSBC%20Global%20Private%20Banking%20-%20Diwan-i-Aam,%20Red%20Fort,%20Delhi.jpg)

Asia’s Rising Tigers

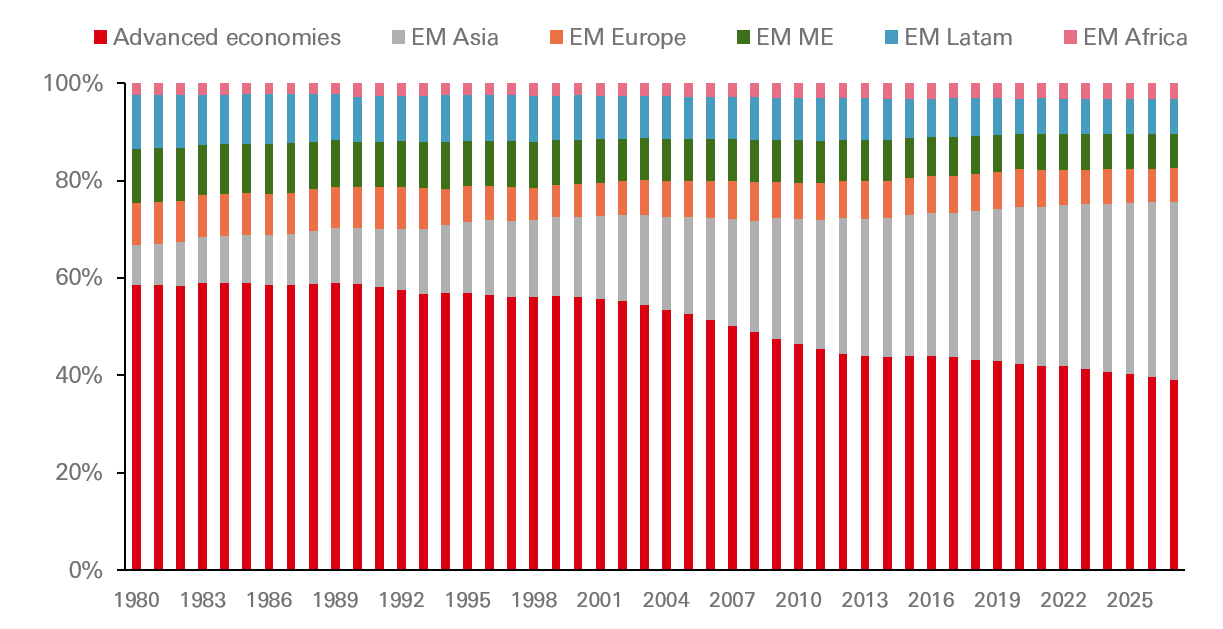

Amid the global slowdown, Asia’s economic momentum stands out by delivering resilient growth, and the easing inflation can support Asian central banks to end the tightening much quicker than the Western banks. Asia already accounts for more than a third of global GDP (as can be seen from the below graph), and that share continues to grow. The initial rebound was led by China’s consumption-led recovery and policy stimulus. But, as this growth seems to be more gradual, we shift our focus to Asia’s Rising Tigers.

Source: IMF, HSBC Global Private Banking, May 2023. Forecasts are subject to change. Past performance is not a reliable indicator of future performance.

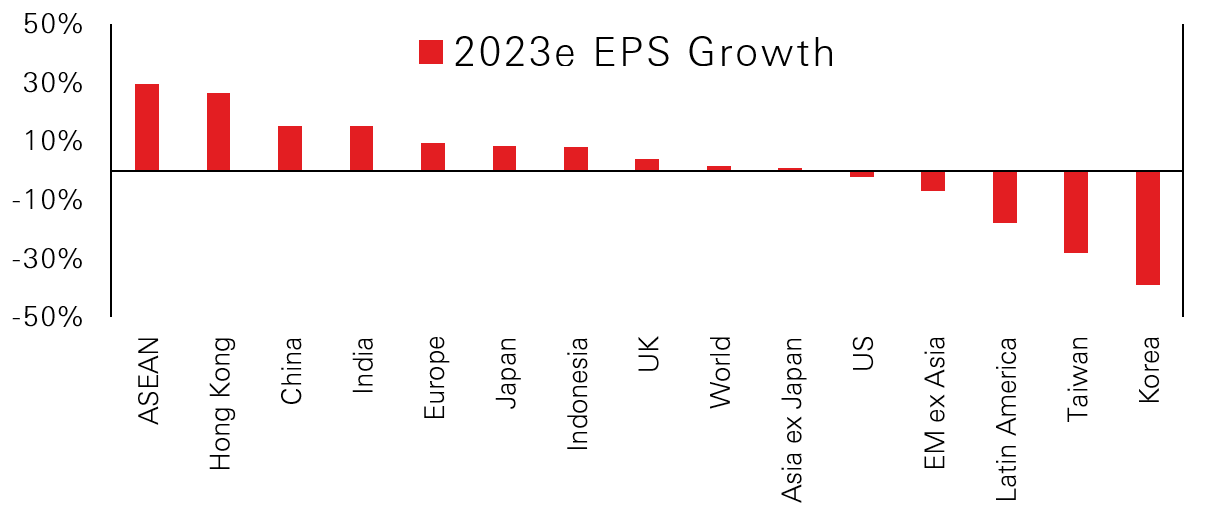

EPS growth opportunities in ASEAN, Mainland China and India are higher than many other economies, as can be seen from the below graph, and hence we maintain our full overweight on Asian equities.

Source: Bloomberg, HSBC Global Private Banking, June 2023. Past performance is not a reliable indicator of future performance.

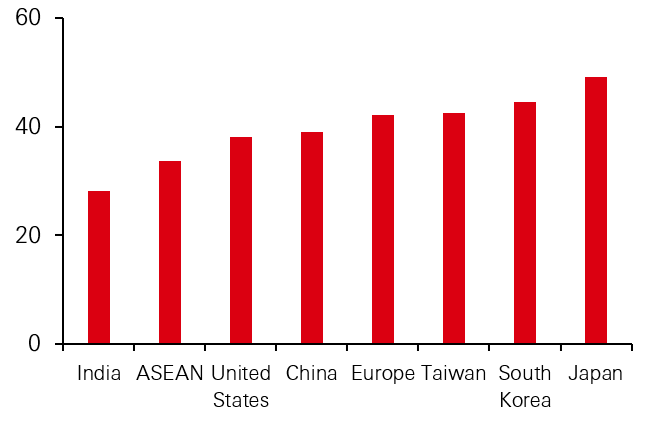

Benefits from the young demographic and rising penetration of the digital economy can drive growth in Asian economies. ASEAN and Indian economies enjoy demographic tailwinds as they have one of the youngest populations in Asia, which will accelerate future growth as more population enters the workforce and drives up domestic consumption. The median age in India and ASEAN is around 28 and 33 years, respectively, which compares favourably to the median age of over 40 in many other developed countries (see below graph). They will be some of the fastest-growing economies in the world. According to Google, Southeast Asia’s digital economy is predicted to reach USD330 billion by 2025 from USD200 billion in 2022.

Source: United Nations, Department of Economic and Social Affairs, Population Division (2022), HSBC Global Private Banking, June 2023

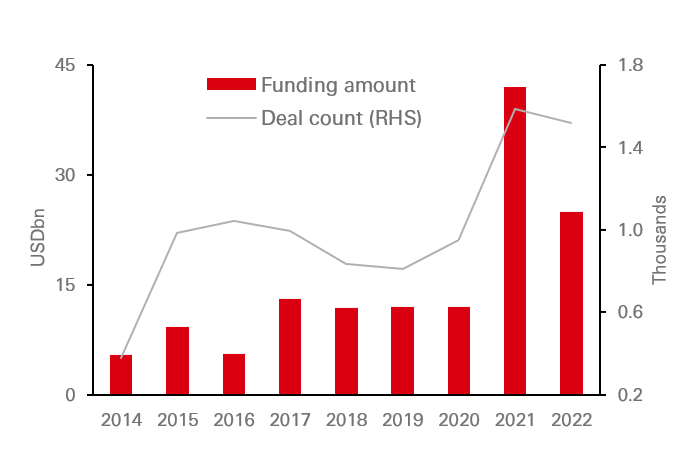

India is one of the fastest-growing economies in the world, posting over 5 per cent average GDP growth for the past decade, and this momentum is only set to accelerate as it reaps the benefits of its favourable demographic dividends. The main trends behind India’s growth story would be the digital economy, high-tech exports and startup ecosystem. As India’s middle class rises, overall consumption could more than double to USD4.9 trillion, and India could become a USD1 trillion digital economy in the next five years. The startup ecosystem in India is on an upward trend and has become the 3rd largest startup ecosystem, producing 1 in every 10 unicorns globally and a total of 107 so far, with a total valuation of USD341 billion. This has attracted significant inflows, thus contributing to job creation, new investment opportunities and growth.

Notwithstanding a temporary lull, India’s dynamic start-up ecosystem has strengthened of late, as can be seen from the below graph.

Source: HSBC Global Research, HSBC Global Private Banking, June 2023

ASEAN economies offer a balanced regional mix to navigate global macro uncertainty, with Indonesia more driven by domestic demand and Singapore more externally oriented. Inflation is moving towards central banks’ targets, implying that we may see less restrictive monetary policies. We see opportunities in consumption leaders that can benefit from an expansion of the middle class, banks that can ride on the ASEAN growth story, as well as the infrastructure sector. Allocation of India in a global portfolio can help increase diversification as Indian equities have a lower correlation to DM than other EM markets, due to its larger domestic economy which is closely linked to its strong structural growth opportunities. In Indonesia, economic retail sales and consumer credit is picking up. The government has also restored fiscal discipline. Supply-side reforms have kept the volatile food inflation in check while also benefitting from strong capital inflows, especially foreign inflows witnessing substantial growth.

Our strategy is to take more broad-based exposure to Asia by highlighting the three biggest domestic markets (Mainland China, India and Indonesia) as our three key overweight positions. Hong Kong should also benefit from increased regional growth, and our upgrade of South Korea from a mild underweight to neutral further broadens our Asian exposure.