M&A in 2022 – what should investors watch out for?

After a record-breaking 2021, what does 2022 hold for mergers and acquisitions?

2021 saw economies reopen and pent-up demand from 2020 led to what Mark Berrisford-Smith, Head of Economics at HSBC UK, describes as a “flurry of activity” in mergers and acquisitions. “In the UK, the certainty of having a trade deal in place with the EU was another factor that prompted interest, especially from foreign buyers,” he continues.

In addition, says Khush Purewal, M&A Partner at KPMG, businesses were closely watching the timing of the announcement of changes to Capital Gains Tax, which saw “a lot of people bringing transactions forward”.

The year ahead

So much for 2021, but what about the outlook for the year ahead? Well after that rush of activity in H1 2021, there was a natural slowing. “By the time you get to late Summer and into September, the number of deals is running at about 60 per cent of what it was in March 2021,” says Mark.

But, says Khush, it’s important to see that in the context of a market playing catch-up and then settling, rather than a dip.

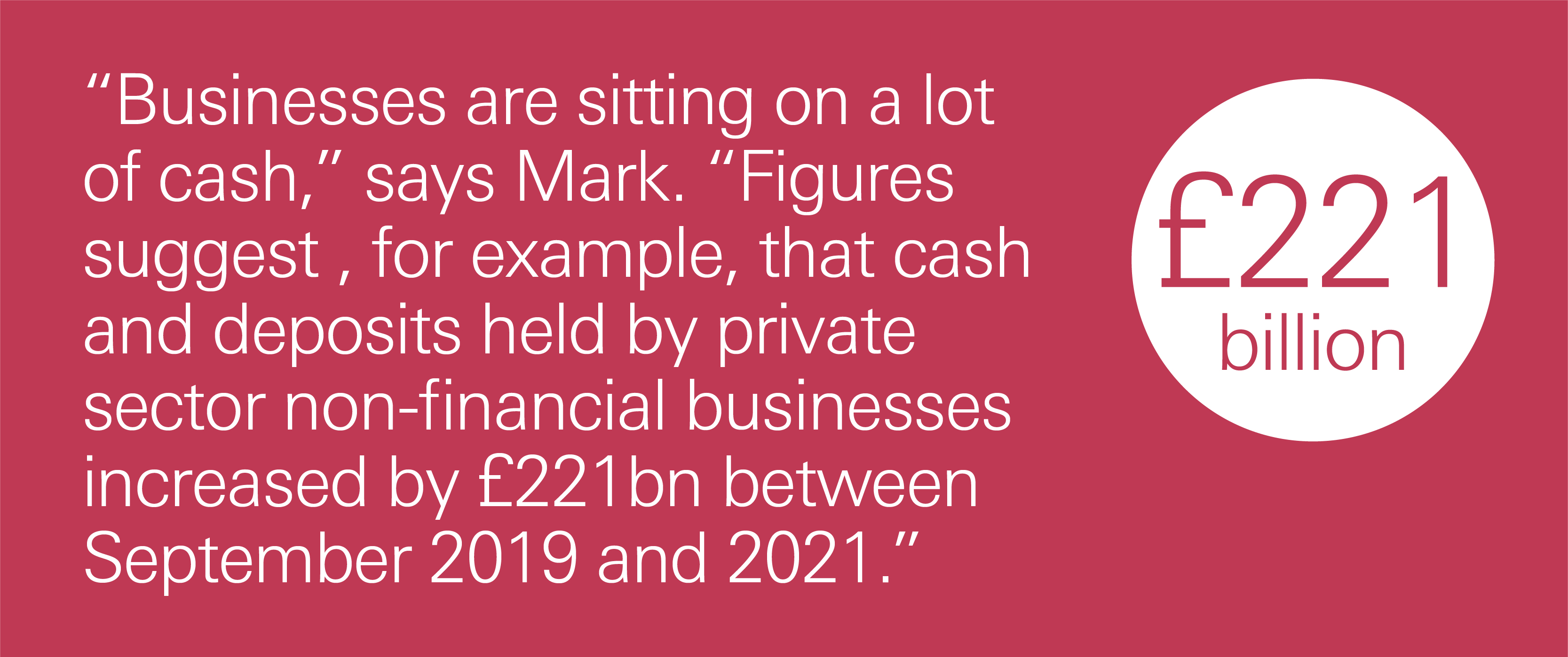

High levels of cash

There are a number of factors driving that optimism.

With funds at their disposal, many of the larger corporates are competing for market primacy, says Khush. “If they need to be in X country or have X technology, and it would take them two years to build or achieve that organically, they’re not going to wait – they’re just getting on and doing the deals.”

And, back to Mark’s point, he agrees that there are high levels of cash through the market, adding that in addition to companies’ own cash piles, there is also a huge amount of capital available from private equity houses. “Most would say we’re at the high watermark of capital raised by private equity, and that money is normally raised with a shelf-life, so there’s a massive pent-up need to spend the money.”

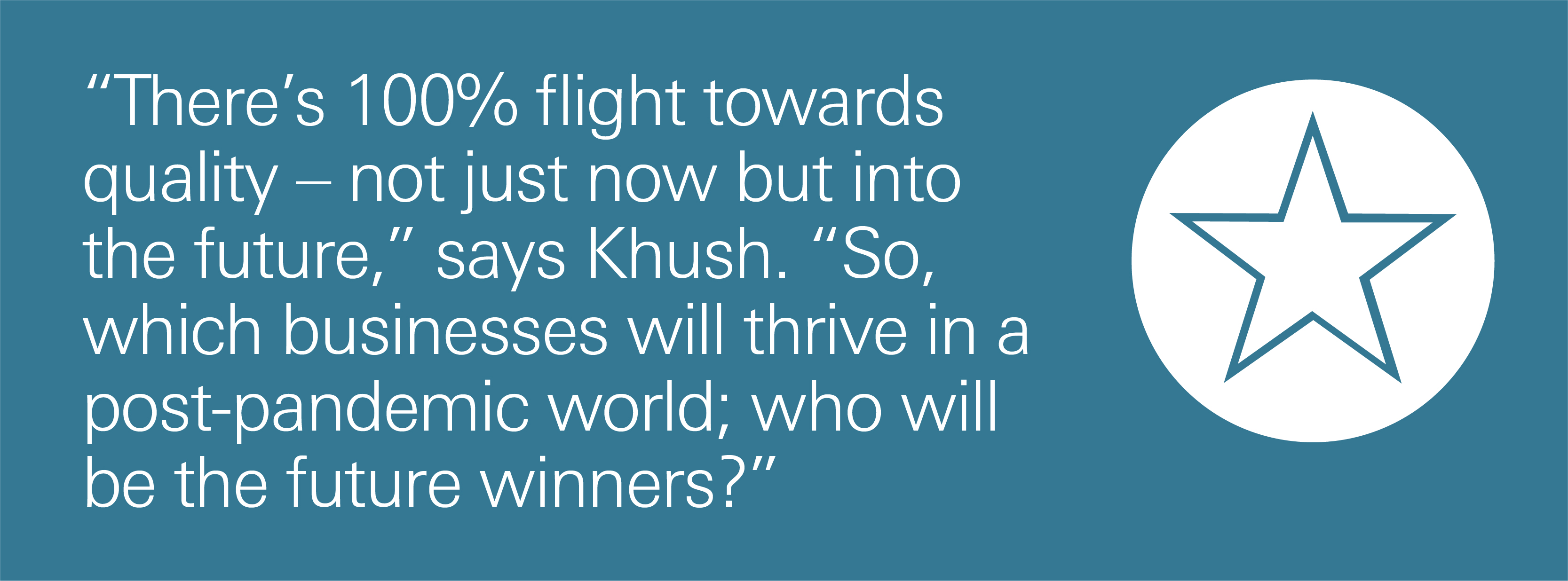

Focus on future quality

However, that money is being spent in a very disciplined way.

This will inevitably drive up prices for those businesses, but also means that those that aren’t market leaders will need to reset their expectations.

Although Khush sees winners and losers in every sector, Mark points out that there are some trends to watch out for. “Anything around the automated agenda, helping businesses re-engineer for the new environment will be attractive,” he says. “There’s a lot of money and interest out there for sustainability too.”

Global trends

ESG is a trend people can’t afford to ignore, agrees Khush. “You need to be clear where your business is because stakeholders are going to be looking pretty hard at what businesses are doing in terms of the environment, their social responsibility and culture, and governance.”

It’s a market that’s increasingly global says Khush, and many of these themes reflect that, as corporates look to diversify risk and increase market share. “The larger the business, the greater the expectations that your exposure is global, because any one country’s not going to satisfy the growth needed to achieve best in class.”

And, while he asserts that every country is likely to see increased M&A activity, the extent of that will depend on the maturity of the business environment, geopolitical tensions, and the regulatory environment, overlaid with ESG approaches and the pace of pandemic recovery. And that’s inevitably where some uncertainty creeps in in terms of the economic climate and the investment landscape.

A balanced approach

“Many central banks will be tightening monetary policy as we move through the year and fiscal policy will inevitably be less supportive as pandemic relief programmes come to an end,” says Mark.

Despite these potential downsides, Khush ends on a note of optimism: “There’s always uncertainty, but decisions now are much more considered, and diligence is broader, deeper and more informative. People are confident in managing that downside and deploying their capital more sensibly. There’s nothing on the horizon to suggest it’s not going to be deployed at a higher value , at a faster rate.”